Running RiskProfiler

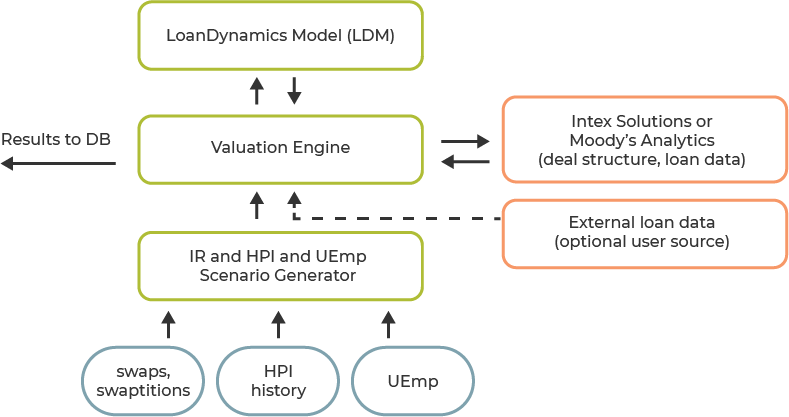

Consider an analysis of a non-agency CMO (right figure). MacroDynamics – which includes both our InterestRateDynamics and HomePriceDynamics models – will produce economic scenarios in accordance with random or specific analyses. The OAS Subroutine will obtain the collateral data, loan by loan from Intex or Moody’s deal files and, for each economic scenario, send it to the LoanDynamics model to produce single monthly mortality (SMM), mortgage default rate (MDR), severity, and delinquency rate forecasts. These vectors will be then passed back to Intex or Moody’s for the necessary aggregation and cash flow generation for the CMO tranche in question. The OAS Subroutine uses these cash flows to compute various analytical measures. Optionally, users may supplement or fully replace loan-level data.

When analyzing MBS and ARM loans or pass-throughs, AD&Co provides cash flow generators Intex/Moody’s will not be accessed). Using an MS SQL database means having a nearly unlimited storage for positions and historical results.