Insights and Takeaways from IMN’s 11th Annual Mortgage Servicing Rights Forum

Andrew Davidson & Co., Inc (AD&Co) proudly sponsored IMN’s 11th Annual Mortgage Servicing Rights (MSR) Forum by Informa at the New York Hilton Midtown. Senior modeler Daniel Swanson joined the “Managing Delinquencies & Forbearance Value” panel in discussing how servicers are adapting to today’s market and the evolving delinquency trends. Rob Landauer, Kevin Lin, and Vivian Li from our Business Development and Financial Engineering teams connected with industry leaders to exchange insights on MSR valuation, risk, hedging, and sensitivity analysis.

Below are some of the themes and takeaways gathered from conversations with attendees and from the AD&Co materials exhibited at the conference.

Rising Delinquency in Recent Vintages

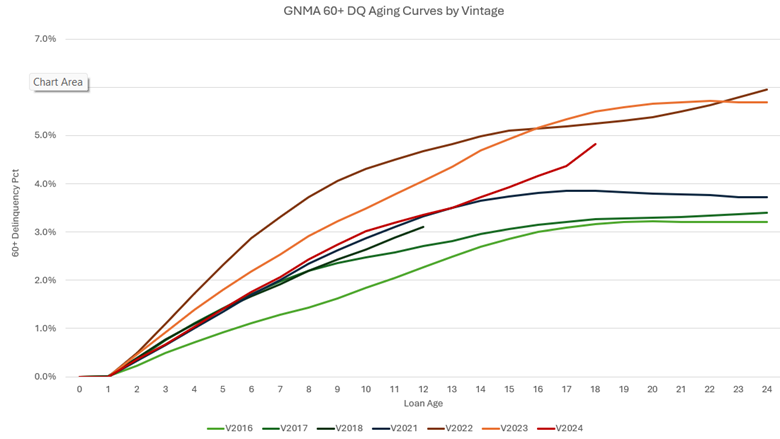

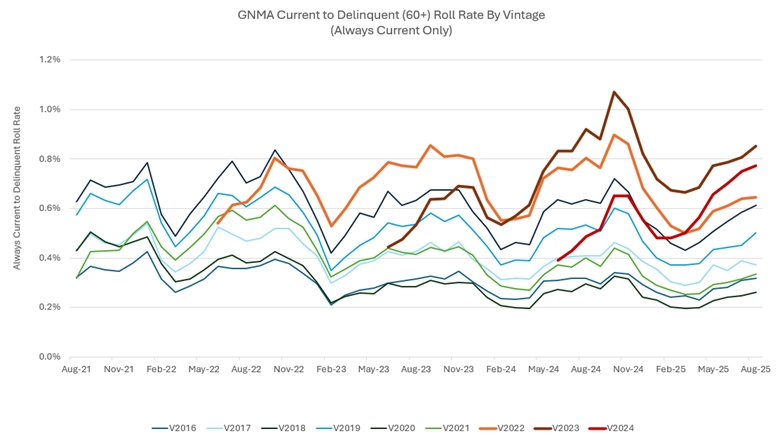

Delinquency was a frequently discussed topic due to increases in delinquency rates in recent vintages. Panelists noted that tax and insurance (T&I) costs continue to increase and along with broader inflation pressures, these factors are driving higher monthly payments; panelists speculated on how much responsibility these higher payments had for the increases in delinquency.

Daniel Swanson shared several slides illustrating this trend, including:

Figure 1. 60+ Days Delinquency Percentage

Figure 2. Roll Rate from Always Current to Delinquent

AD&Co’s LoanDynamics Model (LDM) remains one of our most widely used tools for delivering prepayment and credit analytics. In addition, we recently launched our Climate Impact Suite (CIS), which incorporates climate-related costs — in the form of higher insurance premiums — into borrower behavior (prepayments and delinquencies) and home price appreciation/depreciation projections. First, property-level climate risk data provided by geospatial data vendors is translated into homeowners’ insurance premium forecasts to feed as input to CIS, which then enables users to analyze how these climate-driven payment shocks influence delinquencies, prepayments, and MSR valuations. Homes with substantial equity may see increased prepayment activity in response as cost rises, while lower-equity borrowers may be at higher risk of default.

For more details, see Eknath Belbase, “Introducing Pilot Projects for Climate Impact Suite,” The Pipeline 191 (September 2025).

MSR Valuation and Hedging in the current environment

The relative stability of interest rates over the last few years has created a welcoming environment for new opportunistic MSR investors to enter the market. The increased bid from new investors, along with stable rates, has contributed to strong MSR valuations.

However, a panelist raised an important question: Will these transitory investors remain committed if interest rate volatility increases? Some panelists also highlighted concerns about the politicalization of Federal Reserve monetary policy, with potential rate decisions influenced by political considerations rather than inflation and employment mandates. Rate and political uncertainty could put downward pressure on MSR values.

Some companies leverage MSRs as a natural hedge to their loan origination business. Some companies deploy extensive hedging with 100% of the MSR book hedged to control convexity risk. A new hedge instrument, SOFR Swap Futures from Eris, was discussed as an alternative to TBAs and other current hedge instruments because it more directly tracks SOFR risk and provides more efficient use of capital versus swaps.

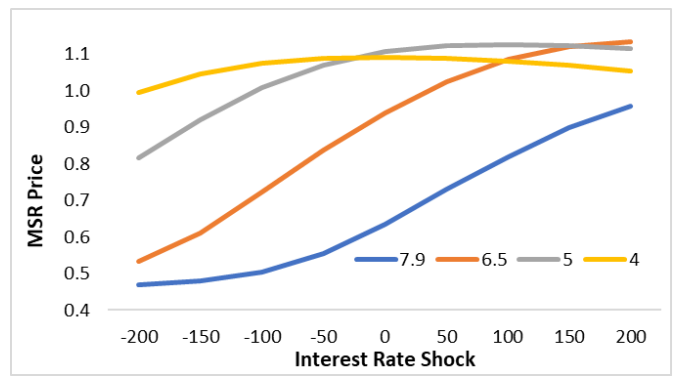

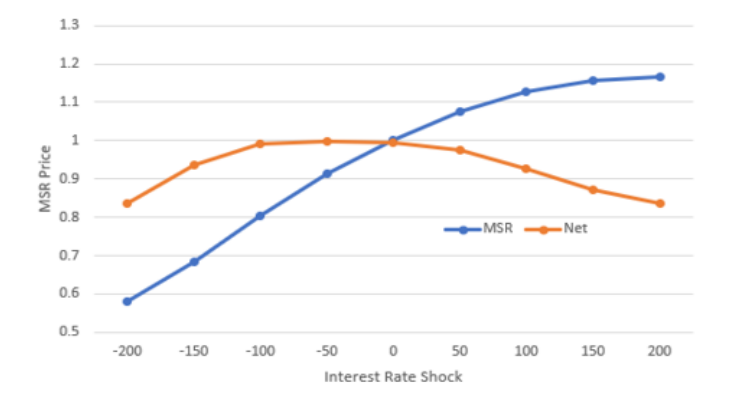

AD&Co’s Mortgage Servicing Rights Kinetics (MSRK) platform allows users to value servicing assets, visualize rate-risk dynamics, and evaluate hedge strategies.

During the conference, we set up MSRK demos in our booth, highlighting:

Rate-shock sensitivities from –200 bps to +200 bps on MSRs for note rates from 4% to 7.9% (Figure 3).

-

Results emphasized the importance of hedging par and premium MSRs against rising-rate scenarios.

A hedge example applying TBA swap to a 6.7% MSR (Figure 4).

-

The TBA swap overlay helped flatten returns across rate paths and stabilize value.

Figure 3. Impact of Interest Rate Shocks on Different MSR Note Rate Prices

Figure 4. GSE 6.7% MSR: Interest Rate Shocks with TBA Swap

Highlighted topics:

Recapture

Recapture remained one of the most prominent themes—continuing the strong focus seen at last year’s forum. Industry participants highlight recapture as a critical component of MSR valuation and bidding, as market participants are assigning up to a 20% value to this factor. AI and related marketing efforts have put customer retention/recapture at a four-year all-time high. Failure to incorporate the value of recapture in an MSR bid will likely lead to failure. Further, high WAC loans can be more valuable MSR as the refinance propensity generates recapture value.

50-year mortgages

Recently, the administration drew national attention to 50-year mortgages, framing them as a pathway for home affordability and lower monthly payments. The general consensus among conference participants was that 50-year mortgages offer little in the way of promoting home affordability as the increase in overall interest paid by borrowers over the life of the loan more than offsets the relatively modest savings in monthly Principal & Interest (P&I). There were concerns regarding the credit profile of borrowers who cannot qualify for 30-year mortgages but could qualify for 50-year terms. Such products may introduce market distortions or unintended consequences for both credit performance and mortgage securitization markets.

Conclusion

This year’s IMN MSR Forum brought together a wide cross-section of the mortgage servicing ecosystem, fostering discussions on delinquency trends, climate impacts, evolving valuation practices, new policy developments, as well as other topics such as technology, credit score, and more. AD&Co was grateful for the opportunity to participate, share our analytics, and engage with clients and partners. We look forward to continuing these conversations in the months ahead.