Ability-To-Repay Benchmark Update

Summary

In 2021, Andrew Davidson & Co. Inc. (AD&Co) proposed a benchmark cohort approach to setting Ability-to-Repay (ATR) Qualified Mortgages (QM) standards. Successful benchmarks based on data are model-free and transparent, and the cohorts must perform consistently in comparison to one another and across time. Our original work used data through the early stages of the pandemic when non-performing loan percentages skyrocketed. This update shows that the cohorts continue to perform consistently.

To review; the metric is 60+ DQ (delinquency) rates at 24 months old for loans guaranteed by GSEs, FHA, VA, and non-QM securitizations. We update performance through late 2021 or early 2022 depending on the data source. The update turned out to be six to nine months past the peak non- performance rates (60+ DQ + Forbearance) of the pandemic. One of the best tests of reliability are cohorts that perform consistently at significant turning points. We show two different examples of cohort performance which all pass with flying colors.

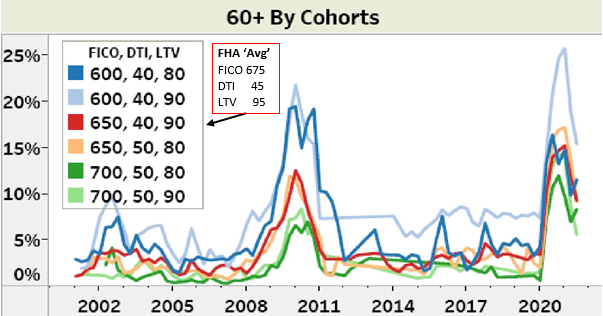

Figure 1 extends the original time-series delinquency graph by cohort across combined federal segments (GSE, FHA, VA) and shows consistent performance through the two sharp turning points in delinquencies from the lows before the pandemic and the peak thereafter.

Figure 1. Delinquency Rates by Cohort

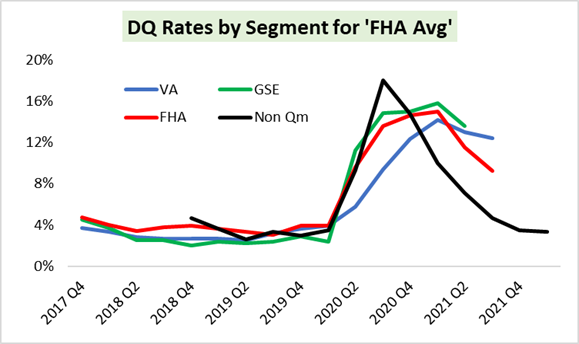

Figure 2 extends the time-series graph that compares the ‘FHA Average’ cohort for each of the three federal segments, GSE, VA, FHA, and non-QM. The ‘FHA Average’ cohort is roughly 95 LTV, 680 FICO, 40 DTI for government lending, and about 90 LTV, 680 FICO for non-QM. The results continue to illustrate that the benchmark cohorts perform consistently across market segments.

Figure 2. Delinquency Rates for ‘FHA Average’

Conclusion

The pandemic and the federal response to it are unprecedented in modern times for their impact on the US economy and housing market. Nevertheless, mortgage cohorts performed consistently over the last several years across federal and non-QM segments, increasing confidence in this approach. This stability contrasts with the vastly higher non-performance rates of the subprime and reduced documentation era that resulted from poor lending practices, as we reported in the original study.

This highlights that conscientiously measuring income is essential to consistency.