Combatting the Effects of Algorithmic Bias

Homeownership is the largest source of wealth accumulation and inter-generational wealth transfer for the working and middle class. However, the history of racial discrimination (it was actually legal to discriminate by race in housing until the Fair Housing Act of 1968), suggests that we have a continuing responsibility to ensure fair access to housing and housing finance.

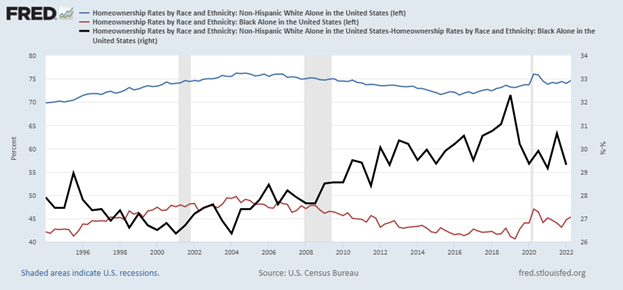

The homeownership rate for white Americans has averaged 70-75% over the last 25 years but only 40-50% for black Americans. In fact, the gap has widened over this period.

What is Equitable Housing Finance, and how do we make progress towards it?

The issues of economic opportunity, and geographic and housing inequality, are long-standing and varied. But as practitioners in mortgage risk and analytics, we focus on data, assessing risk and equal access to mortgage credit. Households of moderate means generally use credit to buy their first home so we must consider credit access and the quantitative process carefully, especially in the context of artificial intelligence and unintentionally biased algorithms.

The premise is simple: Use the same comprehensive set of financial data for everyone and apply it fairly.

Going beyond credit scores

Most people know about credit scores, which serve as the principal metric used for credit decisioning. What if it turns out that credit scores don’t reflect all relevant consumer financial data? What if this data gap has grown over time, and what if it’s larger for targeted groups like minorities and low-income families?

To the degree that mortgage decisioning models omit relevant data, they become less accurate. To the degree that such omissions are concentrated among certain groups, these models will contain algorithmic bias.

Consumer credit scores were created in the 1950s, and the Equal Credit Opportunity Act of 1974 ensured they could not include discriminatory information. The FICO formulation commonly used for mortgage credit today was built about 2004 and it correlates well to the likelihood of short-term delinquency.

However, financial data is now available that is materially relevant to consumer credit performance, but is not included in credit scores. This data is generally more significant for renters and underserved populations, those with smaller traditional financial footprints. Such indicators include consumer credit card balances, telecom/utility payment data, and free cash flow from bank accounts.

The mortgage ecosystem is beginning to work towards using expanded consumer financial data. AD&Co is acquiring this data and improving our analytics make mortgage decisioning both more accurate and more fair.

Working through public policy

Leveraging new data, advancing national standards, and broadly implementing improved decisioning are not automatic. Most mortgage lending is federally connected (GSEs, FHA/VA, banks), and compliance standards are universally applied. This occurs in part because the mortgage market contains inherent information asymmetries and social externalities around fairness and stability. The confluence of finance and policy leads us to combine our analytic efforts with actively engaging with federal counter-parties and in the policy debate. This includes focusing on how to integrate new data sources into mortgage decisioning on a national scale as a means to improve accuracy and fairness.