Drivers of Discount Prepayments

As interest rates rise and fewer loans with refinancing incentive remain, other factors are primed to play a larger role in determining prepayment speeds in the coming months (and perhaps years). Turnover, the rate at which people move, is the most cited of these factors. In this blog post, we’ll consider two other potential drivers: curtailments, or partial prepayments, and mortgage payoffs that don’t involve taking out a new loan.

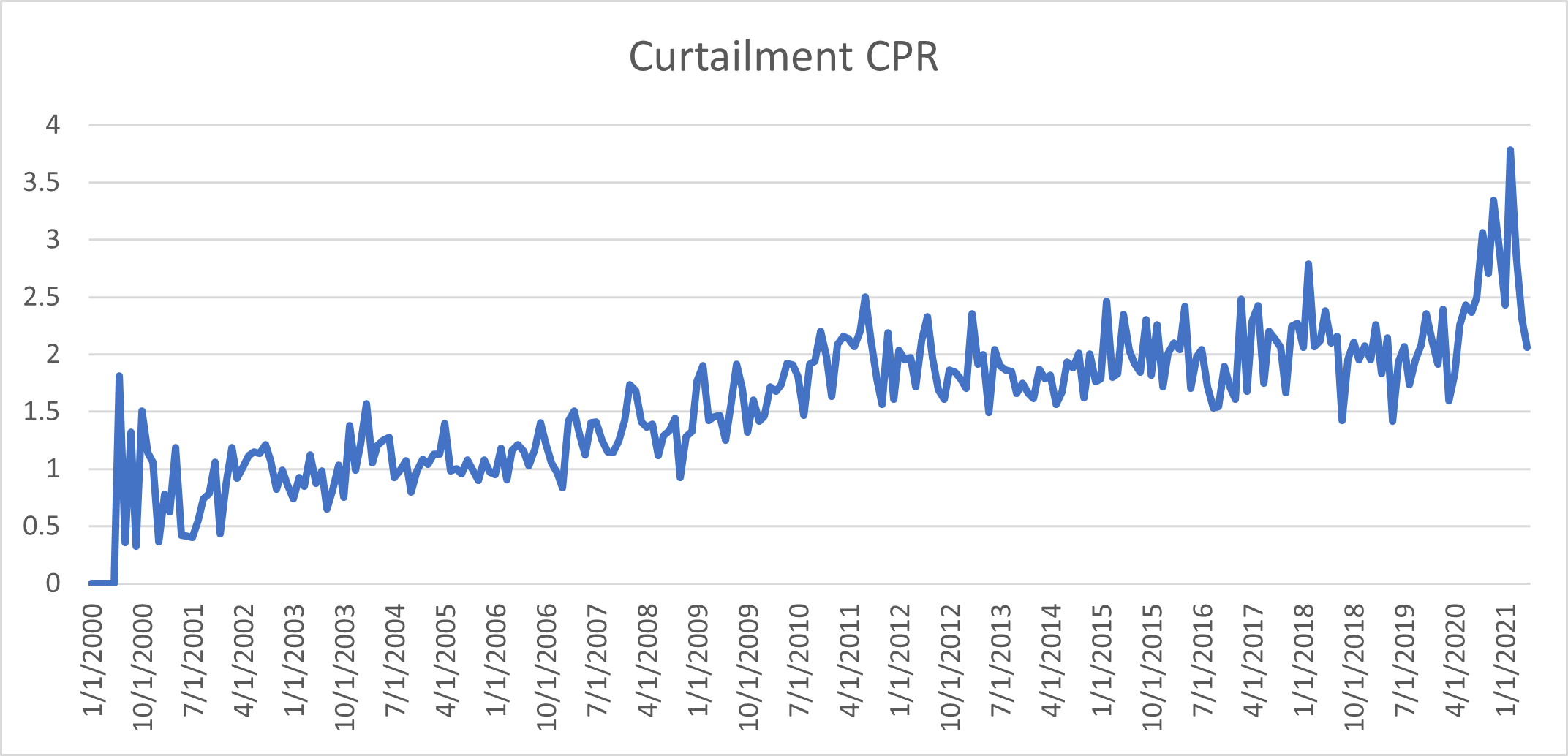

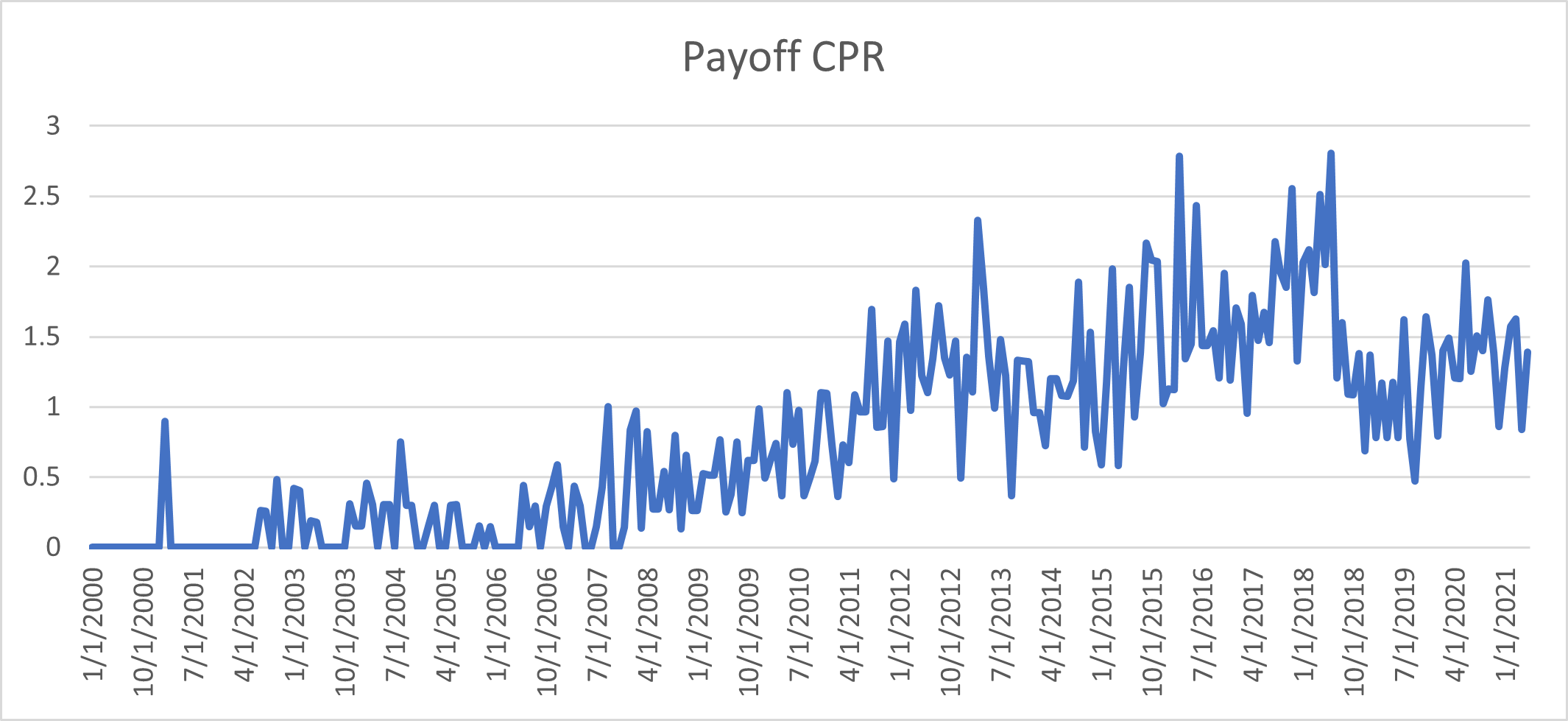

The charts below the rates of curtailment and payoffs in a sample of Fannie Mae loan level data[1].

Curtailments involve borrowers making additional payments beyond their amortization schedule yet short of paying off the full amount, i.e., people making an extra payment each month. In the charts we can see the rate rising slightly over time (which is mainly attributed to age; this data only has loans originated after Jan 1999, so the earlier months are limited to younger loans) and settling into a rate around 1.5-2.5 CPR. However, there was also a bit of a jump during the pandemic, which can perhaps be attributed to borrowers having extra cash from stimulus payments.

Full payoffs involve paying off a mortgage completely without moving or taking out a new mortgage, which tend to occur if borrowers find themselves with enough cash to cover the outstanding balance. While this can’t be known with 100% certainty, we’ve estimated the rate by looking at payoffs with a remaining term of 36 months of less. These are unlikely to be refinances and while we can’t rule out the possibility of the borrowers moving, we observe payoff rates loans with short remaining terms to be dramatically above the baseline turnover level. In essence, this chart shows the percentage of loans with short remaining terms (low) multiplied by their payoff rate (high) to get the overall contribution to CPR. Like curtailment, the data takes a while to ramp up, but then settles into 1-3 CPR range.

Both series represent a small percentage of prepayments in normal environments, but a greater percentage of the overall level in a world without refinancing. While it’s not a given that these numbers will remain constant in the face of rising rates, it is likely that these factors won’t have quite the same sensitivity to rates as refinancing (this study found payoffs to be relatively flat at negative incentive[1]). If rates stay high, it may be useful to keep these factors in mind moving forward.

[1] https://www.philadelphiafed.org/-/media/frbp/assets/working-papers/2019/wp19-39.pdf

[1] https://capitalmarkets.fanniemae.com/credit-risk-transfer/single-family-credit-risk-transfer/fannie-mae-single-family-loan-performance-data