FRED Adds AD&Co’s GSE-and-Borrower-Option-Adjusted Spreads for CRT Indices

AD&Co US Mortgage High Yield Indices

The Federal Reserve Economic Data (FRED) portal, housed by the Federal Reserve Bank of St. Louis, has been publishing AD&Co’s CRT indices since 2019. These series posted under the overall name of “US Mortgage High-Yield” include total return rates and credit and option-adjusted spreads (crOAS) – a projected return’s spread over Treasury (in the past, Libor). These series are available going back to 2014-end and tiered by CRT initial supports.

Tier 0 includes all CRTs with under-25 bps support; Tier 1 bonds have supports exceeding 25 bps, but not 95 bps; Tier 2 has support from 95 bps to 175 bps; Tier 3 – from 175 bps to 375 bps, and, finally, Tier 4 – above 375 bps. The actual bond’s name (As, Ms, or Bs) that matches each tier can vary over time and between Fannie Mae’s CAS and Freddie Mac’s STACR transactions. We define Mid-Tier as the aggregation of Tiers 1 through 3. A CRT to be included in an index must have a factor of 0.25 or higher.

While actual rates of investment return are computed model-free, crOAS levels come from the AD&Co model. Importantly, the crOAS indices that date back to 2014 do not account for the GSE call option embedded in a CRT and therefore overstate the expected return. See, for example, index CROASMIDTIER for Mid-Tier or index CROASTIER0 for Tier 0; the latter currently shows crOAS of about 600 bps.

What is New?

Over the last couple of years, AD&Co developed a model to account for embedded GSE calls. Most CRTs are now issued with a five-year call and a cleanup call. Exercised in the interest of the GSEs, those options reduce investor return. Our December 2024 Quantitative Perspectives[1] laid out the theoretical foundation of our methods. A subsequent September 2025 Pipeline article[2] listed results of the production analysis across the entire CRT cash market.

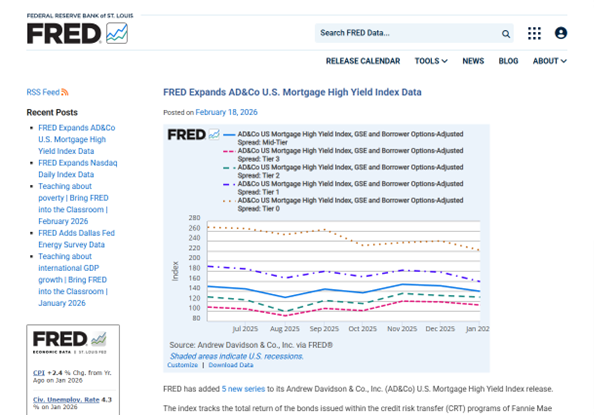

We have been using the new method in our CRT Monitor monthly publication for the last several months. We have also started sending the new series to FRED, which has adopted it with an announcement. The new crOAS series goes back only to June 30, 2025, and is reported by the same tiers as the previously computed ones. To indicate the difference in the series, the new series contains “GSE and Borrower Options-Adjusted Spread” in the names. A screenshot of FRED’s onboarding, showing all the indices together, is seen below.

As expected, the more protected CRTs are priced at tighter, more realistic, crOAS levels. They never reach many hundreds of basis points when the GSE option is accounted for.