Takeaways from Lessons Learned: Insights for Managing the Interest Rate Risk of Banks

Andrew Davidson & Co., Inc. (AD&Co) held a webinar on June 8th entitled “Lessons Learned: Insights for Managing the Interest Rate Risk of Banks.” Mickey Storms from our Alliances and Policies team, Alex Levin from our Financial Engineering team and Andrew Davidson were featured speakers.

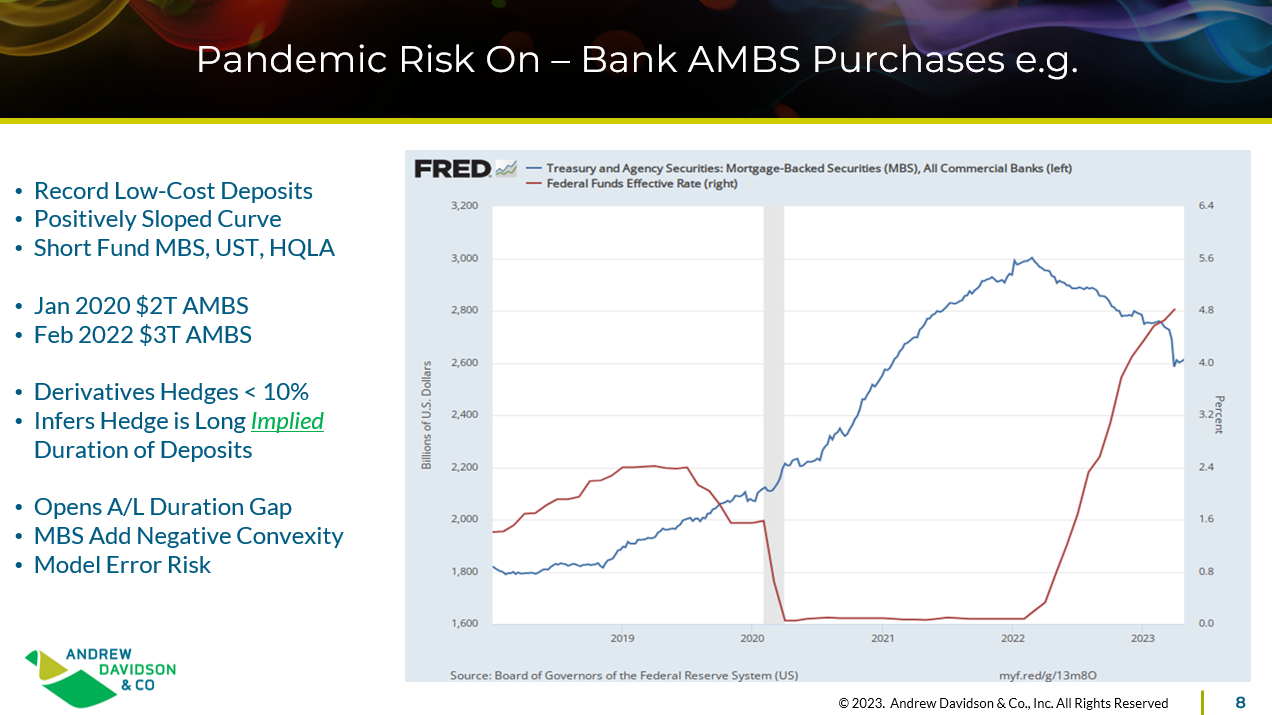

Mickey revisited interest rate changes since the onset of the pandemic and showed how these led to changes in appetite for yield curve risk at banks as interest rate declines compressed their Net Interest Margins (NIM) as depicted in the slid below. He went on to show how this appetite conveyed a questionable sense of comfort by banks that the Assets and Liabilities (A/L) duration gap would not be problematic in the future. The example presented was the strategy of increased short funding of MBS with deposits as rates fell during the pandemic, the success of which depended on an implied long duration of deposits to conceive of a manageable duration gap between A/L. He went on to show the significant duration that exists on the asset side of bank balance sheets and that in the absence of hedging, the success of short funding strategies relies critically on the behavior and duration of deposits whose behavior has changed recently. Mickey closed by pointing out that there has been a lack of regulatory focus on Interest Rate Risk (IRR) in recent years that accommodated banks taking interest rate and duration risk at U.S. Banks.

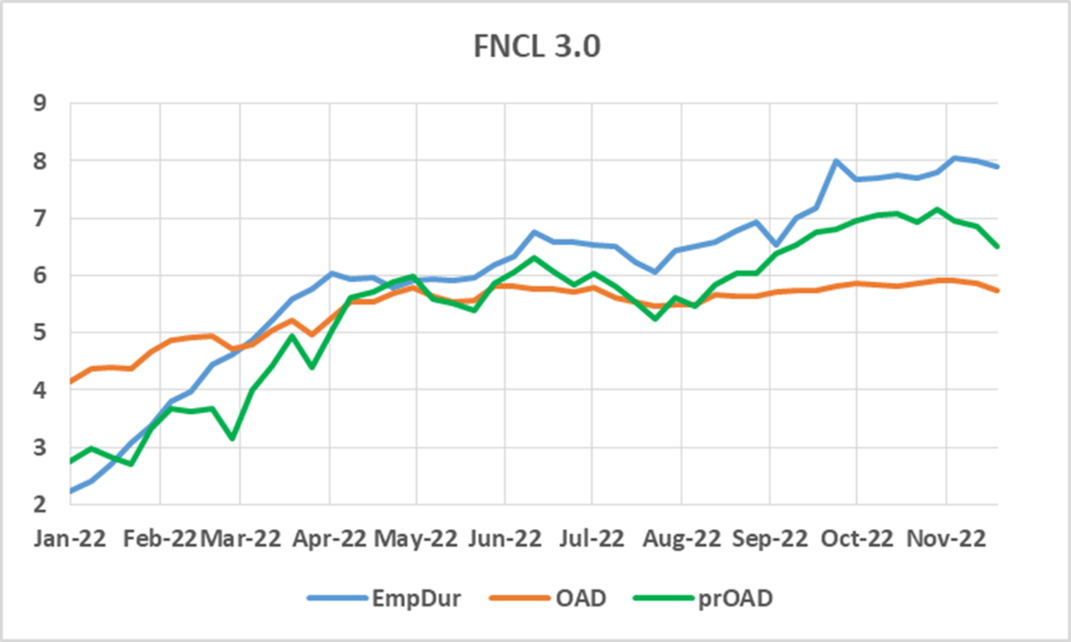

Alex considered several important methodological challenges in measuring IRR and the A/L duration gap. He began with the asset side and explained why an empirically developed prepayment model is not sufficient to fully capture AFS assets’ market sensitivities. For the purpose of replicating those sensitivities, a prepayment model needs to be “risk-neutralized” with faster refinancing and slower housing turnover – the main feared directions of the prepay-model risks. A risk-neutral model would better track market sensitivities of premium and discount assets, as illustrated by the dynamics of different duration measures during 2022 (a similar pattern observed across the TBA coupon stack).

As a risk-neutral turnover rate is slower than an actually observed one, the currently outstanding MBS portfolios (and most banks’ assets) are longer (duration-wise) than many people think.

Comparative Duration Measures

OAD – Option-adjusted duration utilizing empirically developed prepay model

prOAD – Option-adjusted duration utilizing risk-neutralized prepay model

EmpDur – Empirical 60-day sensitivity measured from the daily moves of TBA price and 10-yr rate (model-free)

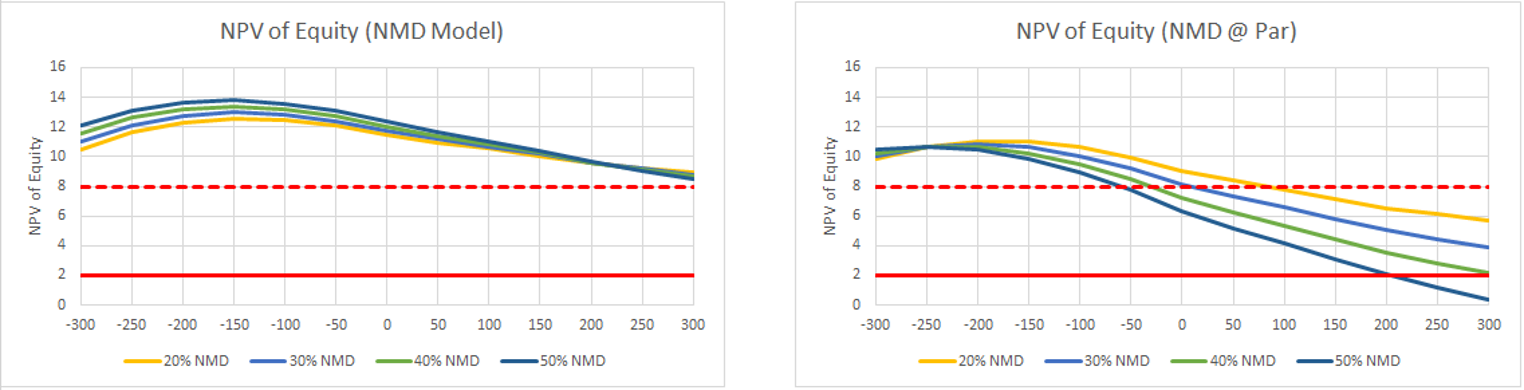

Alex discussed the role of Non-Maturing Deposits (NMD). While an empirically defensible model of retention and paid rate is a good start, many external factors are typically not evident from historical data. Those include possible changes in the deposit base or media/bad press effects that could shorten the duration of NMDs. Therefore, A/L duration gaps are likely to be wider than ones measured.

Alex demonstrated a Net Present Value (NPV) analysis of a hypothetical bank with assets, term liabilities, and NMDs. He constructed a TBA-13-type of NPV of equity profile for two cases:

- NMDs are intact (chart on the left below)

- NMDs are replaced with par-valued liabilities having no intangible value to the bank (chart on the right below).

This exclusion of the economic value of NMDs from the NPV consideration is a useful stress-test we recommend banks conduct.

A bank’s hesitation to hedge IRR is commonly linked to a loss of NIM under the commonly steep yield curve. Under the current inversion, swaps have a positive carry that would improve NIM while closing (or even inverting) the duration gap. Alex demonstrated the use of a 3-year SOFR swap that would make the same bank duration-neutral while adding 50 bps of NIM or even inverting the IRR exposure while adding 100 bps of NIM.

Andy closed by dimensioning the two-way risks that exist with respect to future interest rates and the shape of the yield curve and pointed out how this may impact the dynamics of other assets and businesses that banks maintain. Among these were mortgage servicing and origination. He addressed bank risk management board roles, policies, procedures and controls and discussed the critical importance of an open culture with respect to risk insights and tactics. The review of models and scenarios used to manage IRR was also presented, as was the importance of asset diversification and capital allocation processes that include risk limits. He closed by talking about Basel 2 IRR analytical methods and how focusing on economic value, earnings and market are essential to effective IRR management.

Click here to view the presentation and webinar recording.