Welcome to The S-Curve

Now you will be able to receive the latest announcements, product updates, and our insights on the mortgage market in real time.

The name of the blog, the S-Curve, is a reflection of our logo and the central feature of our prepayment model. S-curves are seen in nature in many phenomenon, from population growth to prepayment and default models. Our first S-curve, in the early 1990s, used the arctangent function, then piece-wise linear functions, and evolved over time to be more complex and vary by FICO, loan size and LTV. This evolution encapsulates both the timeless nature of fundamental relationships and constant innovation to describe them better over time.

We hope you find the information useful and we look forward to your feedback.

-

Mortgages at SFVegas 2023Events

Mortgages at SFVegas 2023EventsThe Structured Finance Association hosted SFVegas 2023 (February 26 - March 1), a broad capital markets conference with thousands of attendees in Las Vegas. Andrew Davidson & Co. Inc. (AD&Co) was a sponsor focused on the mortgage sector. As we engaged with clients and policy leaders, a few themes emerged: Data, Expanding Access Safely, Ginnie Mae Servicing and Auto Loan Performance.

Data

Well-managed data is the underpinning of well-run mortgage organizations, supporting efforts to manage risk, profitability, and compliance. Data is essential to developing new products, improving accuracy, and expanding access to mortgage finance. Nearly everyone we spoke to spends time and money on data and still struggles to manage it through their internal operations, from loan level acquisition to portfolio management and reporting. They expend additional effort to acquire and pass on data in the larger mortgage ecosystem. The richness and reliability of data degrade even within companies, let alone as mortgage-related assets pass through the value chain. This degradation worsens the information asymmetry between sellers and buyers, increasing risk and pushing the mortgage business further from an efficient market. It impedes adding new data to the data-frame, such as the new Trended Credit Scores or expanded data generally, that helps expand markets.

These realities align with the economic theory of imperfect markets and utilities. Markets that provide gains from scale and consistency have attributes of public utilities. Adding privacy concerns and positive systemic value beyond individual mortgage transactions do as well. Reducing the inherent information asymmetry between sellers and buyers further suggests that the efficient market outcome could be a regulated market utility of loans and related data. Data aggregators can supply to the utility, and data consumers can access it.

Expanding Access Safely

Safely expanding access to mortgage finance is not automatic. The legacy of discrimination generally and in housing finance specifically, shows up in the persistently lower homeownership rates of minority populations. Homeownership rates can be expanded temporarily by lowering standards and raising risk, or durably by using new data that lowers risk. Making progress requires commitment and solving the data market failure described above.

Ginnie Mae Servicing

It’s well known that compliantly servicing non-performing loans can cost several times the fixed servicing fee and thus pose systemic risk. During the Pandemic, Federal agencies scrambled to provide financing and reduce the burden on non-bank servicers that represent a substantial majority of the Ginnie Mae market without the federal backing that most of the mortgage ecosystem enjoys. This cost-revenue imbalance is not an advancing issue and cannot be solved by transferring the burden of advancing NPL payments to bond holders. The market bid for Ginnie Mae servicing in mid-2020 was zero because of the expectation of high NPL rates. Fortunately, record low mortgage rates and record refinancing volume provided servicers who were also originators with cash flow to offset the cost of servicing FHA NPL rates that temporarily reached 14%. The next time there is a systemic rise in delinquency rates, this extra cash flow is unlikely.

What’s the solution for this? The most straightforward solution is a variable servicing fee that aligns revenues with expenses, but there is surprisingly little enthusiasm for this solution. Ginnie Mae’s leadership is clearly aware of the systemic risk potential and is seeking a solution. The U.S. mortgage market often uses a federal backstop behind private financial markets to provide the stability the economy depends on. The backstops of deposit insurance or for the GSEs are examples. We will be studying this issue.

Auto Loan Performance

For the first time in awhile, attention is being paid to rising auto loan delinquency rates, both prime and subprime. Ordinarily, today’s historically low unemployment rate would associate with low delinquencies, so this rise is worrisome. It’s well-known that supply-chain disruptions during the Pandemic caused spikes in new and especially used car prices. Cars financed at those high prices pose more risk, and used car prices have already dropped about 15% from their peak. AD&Co will be monitoring this performance and refining our models.

-

Introducing the Kinetics LoanDynamics ModuleProducts

Introducing the Kinetics LoanDynamics ModuleProductsAndrew Davidson & Co., Inc (AD&Co) is pleased to announce the official release of the LoanDynamics Module in Kinetics, AD&Co's new modular platform for running AD&Co analytics via a desktop application, web browser, or REST API. The LoanDynamics Module is the latest way to run the LoanDynamics Model, allowing users to perform sensitivity analysis, validation testing, and scenario analysis in a modern, user-friendly application. The LoanDynamics Module supports all flavors of single-family LDM (Agency, Agency Plus, Non-Agency) and is an alternative to the LDM Excel Spreadsheet.

Users can access the LoanDynamics Module via the Kinetics desktop application (Windows) or a web browser. A developer kit is also available for those who would like to integrate the Kinetics Web Service with their proprietary system.

The LoanDynamics Module joins MSRKinetics and the Auto LoanDynamics Modules on the Kinetics platform. Later on, the Multifamily LoanDynamics Module will become available, allowing users to run agency multifamily loans and securities on Kinetics.

AD&Co always looks forward to your comments and welcomes feedback from frequent users of the LDM Excel spreadsheet, who may have perspectives that will help us improve the new application.

Ready to take the LoanDynamics Module for a spin? Contact us to get started.

LoanDynamics Module Portfolio

LoanDynamics Module Portfolio LoanDynamics Module Scenarios

LoanDynamics Module Scenarios LoanDynamics Module Results

LoanDynamics Module Results -

New Scores in Mortgage ModelsThoughts

New Scores in Mortgage ModelsThoughtsRecently the Federal Housing Finance Agency (FHFA) announced some upcoming changes related to the use of new credit scores, FICO 10T and VantageScore 4.0 by Fannie Mae and Freddie Mac. “FHFA expects that implementation of FICO 10T and VantageScore 4.0 will be a multiyear effort. Once implemented, lenders will be required to deliver both FICO 10T and VantageScore 4.0 credit scores with each loan sold to the Enterprises”.[1] This announcement will impact the entire mortgage ecosystem.

In this blog, I will discuss some of the challenges that come with transforming the analytical models used to value and manage the risk of mortgage loans and securities. Behavioral models are used to forecast the probability of prepayment, delinquency, default, and losses given default. Credit scores are typically inputs into these models. The models in use today are all calibrated using the classic FICO score.

Getting the models ready to run with FICO 10T and VantageScore 4.0 will mean that every single model using these scores will have to be refitted, tested, and validated before they can be put into production. Let us look at what all this entails.

Two populations will be affected by this change:

- Population of new loans

- Population of existing loans and securities

Let’s start with the first population. All new loans will have to be analyzed using FICO 10T and VantageScore 4.0, which means that any origination or risk models for these loans will need to be estimated using the new scores. Underwriters will need to understand the nuances of the new scores and will probably need a mapping from old scores to new scores.

For the second population, we will need to refit the existing prepayment and credit models used by the industry. The new models should take the new scores as inputs. We will need historical data for FICO 10T and VantageScore 4.0 going back at least to the financial crisis of 2008, along with the loan and collateral information. Having data from various economic cycles will be important to parametrize the models with the new scores and validate the sensitivity of the various factors in the models that use the new scores. It would be good to have data from the period leading up to and following the crisis. Pre-crisis will let us quantify the “bad” loans that led to the crisis, whereas post-crisis will let us quantify the delinquencies, defaults, and losses. We also need data for periods when rates went down and when rates went up. With its historically low rates, the pandemic period is a unique period and probably less important from a historical perspective.

Trended data gives us information about a borrower's financial position or liquidity at a given time. A borrower who pays the minimum payment on their credit card debt is called a “Revolver,” while a borrower who makes a full payment is called a “Transactor”. A limitation of the trended data available today is that some major credit card issuers do not report the trended information to the bureaus, which means that the trended scores would have limited training data sets. Is there a way to overcome this bias? Utility data is also not readily available for most borrowers. Fannie Mae and Freddie Mac are now using rental data, but there is no good source of rental data for industry participants.

As we look at new scores, we should also consider how the scores can be made more useful. We know that a borrower’s trended data affects every loan transition throughout the loan lifecycle. Loans could transition from being Current to Delinquent to being Seriously Delinquent to becoming Real-Estate Owned (REO) and finally terminate (and could also transition to prior states). These loan transitions have increased predictive power if we use trended data. The question is, how can industry participants use this information?

This will be a multi-year effort for the industry. It would be better if, for the population of existing loans (about $11 Trillion), we could find an easy way to bridge the existing scores with trended and utility data. Also, as we start using rental, utility, and telecom data, we will have previously unscored loans coming into the ecosystem. There will be a need for frequent model updates as we get additional history about the behavior of these borrowers in various stress environments.

A solution is to use the classic FICO score and use other variables that are orthogonal to the classic FICO score to obtain metrics that are much more predictive through the entire loan lifecycle. A benefit of doing it this way is that we can use loan and collateral information which is not available in a credit score alone. For example, LTV or loan-to-value significantly impacts borrower behavior in stress situations.

We currently do not know a lot about the transition pathway to FICO 10T and VantageScore 4.0 in models used by the mortgage industry. However, one thing is clear. It will take many years before the market is positioned to utilize the advances in analytics coming from new data and new models.

A big question for all market participants is, who will provide the historical data required to recalibrate the models? It is not enough to just have access to the new scores. There should be a way to merge the scores with the collateral and loan data. Fannie Mae and Freddie Mac would be good sources for loans sold to the enterprises, but we would also need data for FHA/VA loans and loans held in bank balance sheets. Also, for the agencies, we would need data for all loans and not just for the loans in the CRT (Credit Risk Transfer) reference data set.

We at Andrew Davidson & Co., Inc. have been working with trended data from Equifax and have found interesting ways to link our prepayment and credit models with the available trended data. It is almost like the next frontier in mortgage prepayment and credit modeling. Models evolve with the availability of new data. Bringing borrower credit bureau data into the modeling process will help us understand and forecast borrower behavior in a much more meaningful way.

[1] https://www.fhfa.gov/Media/PublicAffairs/Pages/FHFA-Announces-Validation-of-FICO10T-and-Vantage-Score4-for-FNM-FRE.aspx

FICO 10T, VantageScore 4.0, and Equifax are trademarks of Fair Isaac Corporation, VantageScore Solutions, LLC, and Equifax, Inc., respectively.

-

The Power of MentoringThoughts

The Power of MentoringThoughtsJanuary is National Mentoring Month which is very appropriate since it coincides with the time when we typically set out our goals and intentions for the New Year. Organizations are embracing mentoring programs and these programs have indeed become a strategic imperative for many. There are many benefits to mentorship and it's easy enough to comprehend. The individuals involved in a mentoring relationship and the organizations that choose to sponsor a mentoring program all are likely to benefit.

For the organization, mentoring can build and strengthen the talent pipeline; help build loyalty among emerging talent; set up or help identify the next generation of talent; and build strategic alignment across silos of an organization by informally encouraging knowledge sharing across different areas. Mentoring programs have proven to be an effective tool to retain and effectively onboard talent, decrease the learning curve for critical roles, build a leadership pipeline, increase employee engagement and build networking and sponsorship. Additionally, mentorship is more frequently being used as a thoughtful tool to promote diversity, equity and inclusion by ensuring that all talent within an organization is provided with opportunities to learn from what the organization may consider to be the 'best and brightest' or simply by those who 'have been there and done that' before. Mentorship promotes diversity of thought and experience to be shared, which we are universally understanding, and recognizing is a benefit to any organization.

For the individuals in a mentorship relationship whether or not they are a part of a formal program, there is unlimited opportunity for learning, growth and development. A mentee has the benefit of getting perspective from someone who can be encouraging but also provide critical and frank feedback when needed and be instrumental in helping a mentee to increase their resiliency in the face of challenges. Mentors can help a mentee to navigate specific situations or people as well as provide sage advice on navigating a career. Solid mentorships can flourish and last for months or years.

Mentorship programs help to connect or match individuals and provide a framework that encourages confidential dialogue on a regular and consistent basis. For organizations -launching, executing and coordinating a mentorship program may seem like a daunting task but it does not need to be. Mentorship comes in all shapes and sizes - the key is to get started. Any company or association should consider providing tools and encouragement for mentorship opportunities both inside and outside of its organization as a simple way to demonstrate that they wish to invest and focus on talent. Talented employees are often looking for opportunities for personal and professional growth just as much as they are seeking promotions and compensation increases. It is important that team members believe they have access to impactful development opportunities to hone their skills and grow into their full potential. Mentorship programs demonstrate a commitment to the employee to develop in the manner they want with goals they establish.

If there is an existing program at your organization, see how you can get involved. If there is no formal mentoring program at your organization then consider helping to build one. In any case, no matter where you are in your personal or professional journey, look for a mentor. And for those of us who are senior leaders look for one or more mentees. I took much pride and enjoyment in starting up a mentorship program at my former company which had hundreds of employees from around the world participate through several "waves" of the program. In addition to opportunities within your company - there are many organizations that seek mentees to volunteer their time. American Corporate Partners (ACP) is a great one that I have had the pleasure of being a part of which helps our veterans, and their spouses prepare for professional opportunities outside of the military. GROW MENTORING is another that I have been a part of which began during COVID-19 by a young lawyer in the UK who simply wished to encourage junior lawyers and law students to connect with more experienced professionals during an otherwise isolated time. University alumni associations, professional organizations such as TechGC and many other groups have mentorship opportunities to get involved in and are always looking for volunteers.

And keep in mind that in a mentoring relationship it's not only the mentee that benefits! Mentorship builds a two-way, mutually beneficial relationship. What mentors learn and take away from mentoring their junior mentees is often priceless and may be the biggest surprise in any mentorship relationship. A good mentor should be an active and open listener. As an active listener a mentor can learn new insights, new values, and tools from their mentee including strengthening their coaching and feedback skills and make important often long-lasting relationships.

Ask most leaders if they have had one or more mentors during their career journey and the answer will undoubtedly be a resounding 'yes'. At a low cost with opportunity for high impact, it is no surprise that mentorship programs are becoming more and more popular, and more and more employees are getting involved. As you set your goals for 2023, I encourage you to seek out opportunities to be a mentor or mentee for yourself and for others.

Happy National Mentoring Month!

-

Combatting the Effects of Algorithmic BiasThoughts

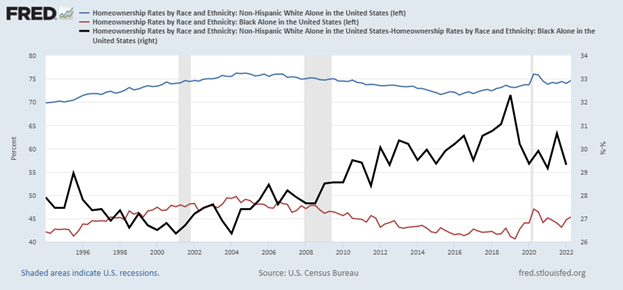

Combatting the Effects of Algorithmic BiasThoughtsHomeownership is the largest source of wealth accumulation and inter-generational wealth transfer for the working and middle class. However, the history of racial discrimination (it was actually legal to discriminate by race in housing until the Fair Housing Act of 1968), suggests that we have a continuing responsibility to ensure fair access to housing and housing finance.

The homeownership rate for white Americans has averaged 70-75% over the last 25 years but only 40-50% for black Americans. In fact, the gap has widened over this period.

What is Equitable Housing Finance, and how do we make progress towards it?

The issues of economic opportunity, and geographic and housing inequality, are long-standing and varied. But as practitioners in mortgage risk and analytics, we focus on data, assessing risk and equal access to mortgage credit. Households of moderate means generally use credit to buy their first home so we must consider credit access and the quantitative process carefully, especially in the context of artificial intelligence and unintentionally biased algorithms.

The premise is simple: Use the same comprehensive set of financial data for everyone and apply it fairly.

Going beyond credit scores

Most people know about credit scores, which serve as the principal metric used for credit decisioning. What if it turns out that credit scores don’t reflect all relevant consumer financial data? What if this data gap has grown over time, and what if it’s larger for targeted groups like minorities and low-income families?

To the degree that mortgage decisioning models omit relevant data, they become less accurate. To the degree that such omissions are concentrated among certain groups, these models will contain algorithmic bias.

Consumer credit scores were created in the 1950s, and the Equal Credit Opportunity Act of 1974 ensured they could not include discriminatory information. The FICO formulation commonly used for mortgage credit today was built about 2004 and it correlates well to the likelihood of short-term delinquency.

However, financial data is now available that is materially relevant to consumer credit performance, but is not included in credit scores. This data is generally more significant for renters and underserved populations, those with smaller traditional financial footprints. Such indicators include consumer credit card balances, telecom/utility payment data, and free cash flow from bank accounts.

The mortgage ecosystem is beginning to work towards using expanded consumer financial data. AD&Co is acquiring this data and improving our analytics make mortgage decisioning both more accurate and more fair.

Working through public policy

Leveraging new data, advancing national standards, and broadly implementing improved decisioning are not automatic. Most mortgage lending is federally connected (GSEs, FHA/VA, banks), and compliance standards are universally applied. This occurs in part because the mortgage market contains inherent information asymmetries and social externalities around fairness and stability. The confluence of finance and policy leads us to combine our analytic efforts with actively engaging with federal counter-parties and in the policy debate. This includes focusing on how to integrate new data sources into mortgage decisioning on a national scale as a means to improve accuracy and fairness.

The S-Curve Archives

-

News

We’re excited to announce a major addition to the Andrew Davidson & Co., Inc. (AD&Co) team. Industry leaders Kelli Sayres and Gene Park, known for building and scaling leading fixed-income analytics platforms, have joined AD&Co’s Business Development team.

-

Thoughts

ThoughtsBuilding on our earlier research on expanded consumer attributes, AD&Co continues to explore how credit data contributes to modeling delinquency and prepayment risk, which are key drivers of mortgage servicing rights cash flows and valuation.

-

Events

EventsAndrew Davidson recently joined NFM Lending’s Greg Sher on the One On One podcast to discuss our recent white paper, “The Impact of Moving Away From the Tri-Merge Standard.”

-

Events

EventsAD&Co recently sponsored and attended SFVegas 2026 and Optimal Blue Summit 2026. This post shares the AD&Co team's unique perspectives and key takeaways from attending both conferences.

-

News

NewsAD&Co US Mortgage High Yield Indices

The Federal Reserve Economic Data (FRED) portal, housed by the Federal Reserve Bank of St. Louis, has been publishing AD&Co’s CRT indices since 2019. These series posted under the overall name of “US Mortgage High-Yield” include total return rates and credit and option-adjusted spreads (crOAS) – a projected return’s spread over Treasury (in the past, Libor). These series are available going back to 2014-end and tiered by CRT initial supports.

-

Thoughts

ThoughtsIn July 2025, the US Federal Housing Finance Agency (FHFA) announced that the government-sponsored entities (the Enterprises or GSEs), Fannie Mae and Freddie Mac, would permit lenders to choose between Classic FICO and VantageScore 4.0 credit score models for loans sold to the GSEs. FHFA also stated in a social media post that the tri-merge standard would be maintained for mortgage underwriting. Nevertheless, some mortgage industry stakeholders recommend moving away from the tri-merge standard for GSE mortgages in favor of a single or bi-merge report standard.

-

News

As housing faces more climate threats that result in more losses, the insurance program that it sits on is teetering on the brink of collapse. Yet, the home insurance market has three distinct stakeholders that have competing priorities, and today, there is no motivation for a collaborative solution.

Understanding how to strengthen and protect the current structure requires looking at the cost burdens along with the risk for each of those parties.

-

Thoughts

ThoughtsThere has been a flurry of activity in the mortgage markets since the 2018 passage of the Economic Growth, Regulatory Relief, and Consumer Protection Act. This act requires the Federal Housing Finance Agency (FHFA, now known as US Federal Housing) to validate and modernize the credit score models used in the housing finance system. It should be noted that so far, the discourse has been around mortgages sold to the Enterprises (Fannie Mae and Freddie Mac). Ginnie Mae has not provided any guidance on their plans to start using new credit score models.

-

Events

EventsAndrew Davidson & Co., Inc (AD&Co) proudly sponsored IMN’s 11th Annual Mortgage Servicing Rights (MSR) Forum by Informa at the New York Hilton Midtown. Senior modeler Daniel Swanson joined the “Managing Delinquencies & Forbearance Value” panel in discussing how servicers are adapting to today’s market and the evolving delinquency trends.

-

Podcast

PodcastTune in to our fourth episode of AD&Conversations with Kevin Lin and Eknath Belbase, our product lead for our Climate model. In this episode, they discuss the new Climate Impact Suite (CIS) pilot project, and Belbase outlines several challenges the team is navigating, including: