Welcome to The S-Curve

Now you will be able to receive the latest announcements, product updates, and our insights on the mortgage market in real time.

The name of the blog, the S-Curve, is a reflection of our logo and the central feature of our prepayment model. S-curves are seen in nature in many phenomenon, from population growth to prepayment and default models. Our first S-curve, in the early 1990s, used the arctangent function, then piece-wise linear functions, and evolved over time to be more complex and vary by FICO, loan size and LTV. This evolution encapsulates both the timeless nature of fundamental relationships and constant innovation to describe them better over time.

We hope you find the information useful and we look forward to your feedback.

-

FRED Adds AD&Co’s GSE-and-Borrower-Option-Adjusted Spreads for CRT IndicesNews

FRED Adds AD&Co’s GSE-and-Borrower-Option-Adjusted Spreads for CRT IndicesNewsAD&Co US Mortgage High Yield Indices

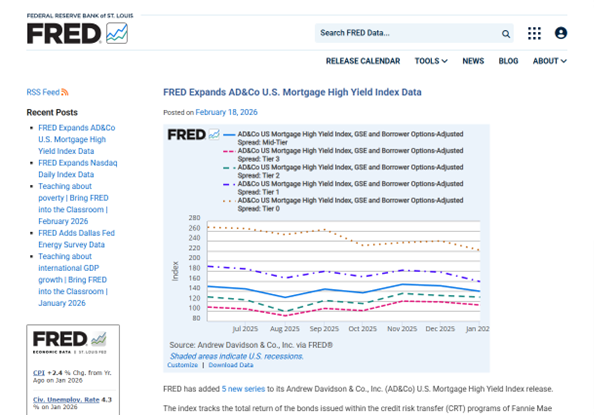

The Federal Reserve Economic Data (FRED) portal, housed by the Federal Reserve Bank of St. Louis, has been publishing AD&Co’s CRT indices since 2019. These series posted under the overall name of “US Mortgage High-Yield” include total return rates and credit and option-adjusted spreads (crOAS) – a projected return’s spread over Treasury (in the past, Libor). These series are available going back to 2014-end and tiered by CRT initial supports.

Tier 0 includes all CRTs with under-25 bps support; Tier 1 bonds have supports exceeding 25 bps, but not 95 bps; Tier 2 has support from 95 bps to 175 bps; Tier 3 – from 175 bps to 375 bps, and, finally, Tier 4 – above 375 bps. The actual bond’s name (As, Ms, or Bs) that matches each tier can vary over time and between Fannie Mae’s CAS and Freddie Mac’s STACR transactions. We define Mid-Tier as the aggregation of Tiers 1 through 3. A CRT to be included in an index must have a factor of 0.25 or higher.

While actual rates of investment return are computed model-free, crOAS levels come from the AD&Co model. Importantly, the crOAS indices that date back to 2014 do not account for the GSE call option embedded in a CRT and therefore overstate the expected return. See, for example, index CROASMIDTIER for Mid-Tier or index CROASTIER0 for Tier 0; the latter currently shows crOAS of about 600 bps.

What is New?

Over the last couple of years, AD&Co developed a model to account for embedded GSE calls. Most CRTs are now issued with a five-year call and a cleanup call. Exercised in the interest of the GSEs, those options reduce investor return. Our December 2024 Quantitative Perspectives[1] laid out the theoretical foundation of our methods. A subsequent September 2025 Pipeline article[2] listed results of the production analysis across the entire CRT cash market.

We have been using the new method in our CRT Monitor monthly publication for the last several months. We have also started sending the new series to FRED, which has adopted it with an announcement. The new crOAS series goes back only to June 30, 2025, and is reported by the same tiers as the previously computed ones. To indicate the difference in the series, the new series contains “GSE and Borrower Options-Adjusted Spread” in the names. A screenshot of FRED’s onboarding, showing all the indices together, is seen below.

Source: FRED As expected, the more protected CRTs are priced at tighter, more realistic, crOAS levels. They never reach many hundreds of basis points when the GSE option is accounted for.

[1] A. Levin and N. Salwen, Valuation of Credit Risk Transfer with Embedded Calls, Quantitative Perspectives, Dec 2024.

[2] A. Levin, Comparative Valuation of CRTs with and without Embedded GSE Calls, Pipeline 191, Sep 2025.

The S-Curve Archives

-

Products

ProductsAndrew Davidson & Co., Inc (AD&Co) is pleased to announce the beta release of a new monthly report series titled “Specified Pool Prepayment Trends,” which aims at showing market prepayment trends for specified agency pools in support of pay-up analyses by investors, traders, and alike.

-

Products

ProductsAndrew Davidson & Co., Inc (AD&Co) is pleased to announce that Polypaths LLC supports AD&Co’s Auto LoanDynamics Model (Auto LDM) providing prepayments, defaults and losses on auto loans and securities.

-

Events

EventsThe Structured Finance Association hosted SFVegas 2023 (February 26 - March 1), a broad capital markets conference with thousands of attendees in Las Vegas. Andrew Davidson & Co. Inc. (AD&Co) was a sponsor focused on the mortgage sector. As we engaged with clients and policy leaders, a few themes emerged: Data, Expanding Access Safely, Ginnie Mae Servicing and Auto Loan Performance.

-

Products

ProductsAndrew Davidson & Co., Inc (AD&Co) is pleased to announce the official release of the LoanDynamics Module in Kinetics, AD&Co's new modular platform for running AD&Co analytics via a desktop application, web browser, or REST API. The LoanDynamics Module is the latest way to run the LoanDynamics Model, allowing users to perform sensitivity analysis, validation testing, and scenario analysis in a modern, user-friendly application.

-

Thoughts

ThoughtsRecently the Federal Housing Finance Agency (FHFA) announced some upcoming changes related to the use of new credit scores, FICO 10T and VantageScore 4.0 by Fannie Mae and Freddie Mac. “FHFA expects that implementation of FICO 10T and VantageScore 4.0 will be a multiyear effort. Once implemented, lenders will be required to deliver both FICO 10T and VantageScore 4.0 credit scores with each loan sold to the Enterprises”.[1] This announcement will impact the entire mortgage ecosystem.

-

Thoughts

ThoughtsJanuary is National Mentoring Month which is very appropriate since it coincides with the time when we typically set out our goals and intentions for the New Year. Organizations are embracing mentoring programs and these programs have indeed become a strategic imperative for many. There are many benefits to mentorship and it's easy enough to comprehend. The individuals involved in a mentoring relationship and the organizations that choose to sponsor a mentoring program all are likely to benefit.

-

Thoughts

ThoughtsHomeownership is the largest source of wealth accumulation and inter-generational wealth transfer for the working and middle class. However, the history of racial discrimination (it was actually legal to discriminate by race in housing until the Fair Housing Act of 1968), suggests that we have a continuing responsibility to ensure fair access to housing and housing finance.

-

Thoughts

ThoughtsDear Friends,

As Andrew Davidson & Co., Inc. (AD&Co) reaches its 30-year milestone, I reflect on two seemingly contradictory ideas: Firms need experience to guide clients through difficult times but sometimes it is necessary to discard past practices to achieve breakthroughs.

-

Thoughts

ThoughtsFor many people, having accessible transportation (a car, for example) is necessary. Most U.S. people live in areas without adequate public transportation and require vehicles to access jobs, healthcare, and groceries.

-

Thoughts

As interest rates rise and fewer loans with refinancing incentive remain, other factors are primed to play a larger role in determining prepayment speeds in the coming months (and perhaps years). Turnover, the rate at which people move, is the most cited of these factors. In this blog post, we’ll consider two other potential drivers: curtailments, or partial prepayments, and mortgage payoffs that don’t involve taking out a new loan.